The Dutch Golden Age

The Dutch Republic in the early seventeenth century was arguably the most sophisticated financial economy on earth. Amsterdam had developed the first modern stock exchange, a central bank, and a culture of investment and speculation unlike anything that had existed before. The Dutch were comfortable with financial risk in ways most of Europe wasn't. They traded futures — contracts for goods not yet produced or delivered. They understood that value could be abstract, built on expectation rather than certainty.

Into this environment came the tulip.

Why Tulips?

Tulips had arrived in western Europe from the Ottoman Empire in the mid-sixteenth century. They were exotic, visually striking, and unlike any flower most Europeans had seen. Certain varieties displayed striking colour patterns caused by a mosaic virus — the very thing that made them diseased also made them beautiful and rare. Among the wealthy, tulips became a status symbol. Prices for unusual bulbs began to rise. Then speculation entered.

A Note on the Evidence

Historian Anne Goldgar's research, published in Tulipmania: Money, Honor and Knowledge in the Dutch Golden Age, cautions that many of the most extreme figures cited in popular accounts of Tulip Mania come from satirical pamphlets written after the collapse — sources with agendas rather than records. The bubble was real. Its scale in popular memory may be somewhat exaggerated.

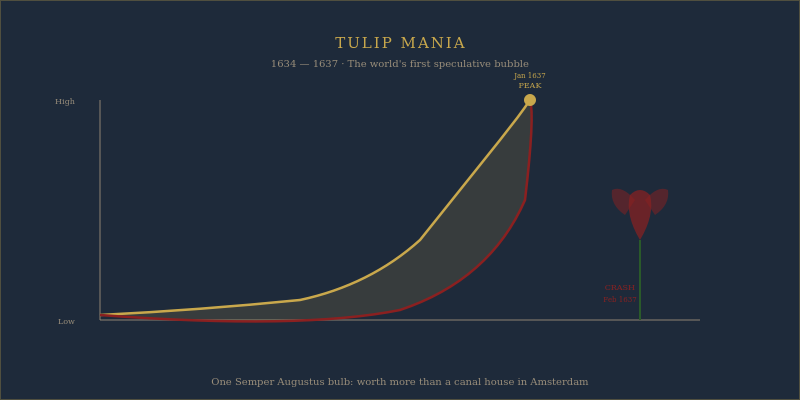

The Bubble Builds

By the mid-1630s, tulip bulbs were being traded before they existed. Buyers purchased contracts for bulbs still in the ground, to be delivered at a future date. This futures market allowed speculation on tulips without ever handling one. Prices rose rapidly. As prices rose, more people entered hoping to profit. As more entered, prices rose further.

The feedback loop felt, to those inside it, like rational behaviour. Everyone was buying. Prices kept going up. Why would you not participate? That question — repeated across every speculative bubble in history — is the mechanism underneath the event.

Tulips arrive in Europe

Tulip bulbs introduced to western Europe from the Ottoman Empire. Become a status symbol among the wealthy.

Speculation begins

Futures contracts for tulip bulbs develop. Prices begin rising rapidly as more buyers enter the market.

Peak of the bubble

Prices reach their highest levels. Some rare bulbs trade at extraordinary prices equivalent to years of wages.

Market collapses

Buyers stop appearing. Prices collapse rapidly. Contracts become worthless. The bubble is over.

The Collapse

In February 1637, the market stopped. The precise trigger is still debated — Goldgar's research suggests it may have begun with a failed auction in Haarlem where buyers simply did not appear. When sellers could not find buyers, prices fell. As prices fell, more sellers rushed to exit. The collapse was rapid.

Contracts became worthless. People who had committed to buying bulbs at peak prices could not find anyone willing to honour the trades. Courts were reluctant to enforce contracts that now seemed obviously detached from reality. The economic damage was real for those directly involved, though the broader Dutch economy remained strong — a detail the popular legend tends to omit.

The Pattern That Repeats

What makes Tulip Mania historically significant is not its scale but its structure. Every element reappears in later financial crises: the novel asset, the rapid price appreciation, the futures contracts, the moment when belief collapses faster than it formed. The South Sea Bubble. The railroad mania of the 1840s. The dot-com bubble. The housing crisis of 2008. Each has its own tulip.

Economic collapse doesn't require a dramatic external event. It requires everyone to stop believing at the same time. And belief is far more fragile than the assets it inflates.

Key Facts

- Period

- 1634–1637, Dutch Republic

- Peak price

- Single Semper Augustus bulb: ~10 times a skilled craftsman's annual wage

- Crash date

- February 1637

- Lasting impact

- First recorded speculative bubble in economic history

Why Tulips?

Tulips had arrived in Western Europe from the Ottoman Empire in the mid-sixteenth century, and by the early seventeenth century they had become fashionable objects of desire among the Dutch merchant class. What made certain tulips particularly valuable — and particularly speculative — was a viral infection that caused the flowers to develop striking multicoloured "flames" of colour on their petals. The infected bulbs, known as "broken" tulips, were unpredictable: a plain tulip bulb might "break" to produce a spectacularly patterned flower, or it might not. This unpredictability became the foundation for speculation.

Timeline of Tulip Mania

The Mechanism of the Bubble

What transformed tulip appreciation into a speculative bubble was the development of futures contracts — agreements to purchase bulbs at a future date at a price agreed today. These contracts allowed people to speculate on tulip prices without actually possessing bulbs. A weaver or a carpenter could participate in the tulip market by agreeing to buy bulbs at harvest time, hoping to sell the contract at a profit before delivery was required.

This futures market operated without any regulatory framework or enforcement mechanism. Contracts were made in taverns, sealed with handshakes, and had no legal standing. The bubble was therefore a purely informal speculative market, which made its collapse both inevitable and swift.

How Serious Was the Crash?

Historians have debated how damaging the collapse actually was. Anne Goldgar's influential revisionist account, Tulipmania: Money, Honor, and Knowledge in the Dutch Golden Age (2007), argues that the bubble has been significantly exaggerated in subsequent tellings. The number of people genuinely affected was relatively small — concentrated among merchants in a few Dutch cities — and the Dutch economy continued to flourish through the seventeenth century despite the tulip crash.

The exaggeration of the tulip mania story is itself historically interesting. The accounts that shaped the popular image of the bubble were written by satirists and moralists who had their own reasons to emphasise the irrationality and excess of tulip speculation. The cautionary tale served ideological purposes.

What remains true is that tulip mania was the first clearly documented speculative bubble in European history, and that its basic structure — rapid price appreciation driven by expectations of further appreciation, disconnected from any fundamental value, followed by sudden collapse — has been repeated in subsequent bubbles from the South Sea Company to dot-com stocks to various cryptocurrency markets.

Frequently Asked Questions

What caused the Tulip Mania collapse?

The precise trigger remains debated. Goldgar's research suggests it may have begun with a failed auction in Haarlem where buyers did not appear. Prices fell, more sellers rushed to exit, and the collapse spread rapidly. The market had been sustained by belief in continued price rises — once that belief faltered, prices fell faster than they had risen.

Did Tulip Mania really destroy the Dutch economy?

Historians including Anne Goldgar have argued the popular account is significantly exaggerated. The trade was concentrated among a relatively small segment of Dutch society and the broader economy remained strong. The damage was real for those directly involved, but economy-wide catastrophe is largely a later invention.

How high did tulip prices actually get?

The precise figures are disputed because many come from satirical pamphlets. Some rare bulbs did trade at extraordinary prices. But the most extreme figures in popular accounts may be unreliable. Goldgar's research suggests the bubble was real but more limited in scope than tradition holds.

Anne Goldgar's Tulipmania: Money, Honor and Knowledge in the Dutch Golden Age makes the case that the conventional explanation misses the social and cultural mechanics underneath the financial story. The full picture is more complex than any short summary can cover.

A Note From The Editor

The most interesting thing about Tulip Mania is not the tulips. It is the question of why intelligent people in a sophisticated economy participated in something that, in retrospect, seems obviously irrational. The answer is that it didn't seem irrational at the time. The feedback loop was real. Prices were rising. The people who got in early had made money. The mechanism that produced Tulip Mania is the same mechanism that has produced every speculative bubble since. The asset changes. The psychology doesn't.